Are you enjoying retirement and looking for ways to save on taxes? Splitting pension income, i.e., transferring part of your income to your partner to reduce your taxes as a couple, is an option worth considering.

This little-known strategy could make all the difference in your budget. In 2023, more than 1,482,000 Canadian couples used this measure to optimize their finances. Let's take a look at how it works and see if you too can benefit.

What is pension income splitting?

Want to pay less tax when you retire? Pension income splitting may allow you to transfer up to 50% of eligible pension income to your spouse on your income tax return.

Note: This refers to private pension income, such as RRIF withdrawals or payments from an employer-sponsored pension. Government pensions (QPP and OAS) are not eligible for this type of splitting.

In practical terms, if you receive more eligible pension income than your partner, you might be able to share that amount when calculating your taxes. This mechanism reduces the taxable income of the higher-earning spouse, allowing them to lower their tax bill. Their partner is then taxed for the transferred amount, who might benefit from a more advantageous rate.

Don't worry. The split exists solely on your tax return. No money changes bank accounts or pockets. You're simply telling the tax authorities to consider part of your income as your partner's, so you can take advantage of their lower tax rate. Your partner may end up owing more tax, but as a couple, you should owe less overall.

How do I know if income splitting is right for me?

The basic principle is simple. Canada has a progressive tax system, so the more you earn, the higher the tax rate applied to the last dollar earned.

Splitting may become advantageous as soon as spouses begin to earn significantly different incomes. If one person earns a lot more than the other, for instance, they probably pay a lot more tax. By transferring part of this income to the person who earns less (and is therefore taxed less), couples can reduce their total bill.

Why should we split pension income?

In addition to reducing taxes, this strategy can offer two other major financial advantages:

- Recover lost credits: Those with very high incomes may see their Old Age Security pensions (OAS) or Age Credits decrease. Reducing your net income through splitting can help recover these amounts.

- Double your pension income credit: Transferring some of your income to a partner who receives no pension would enable them to claim the pension income credit (federal and provincial), thus saving you more.

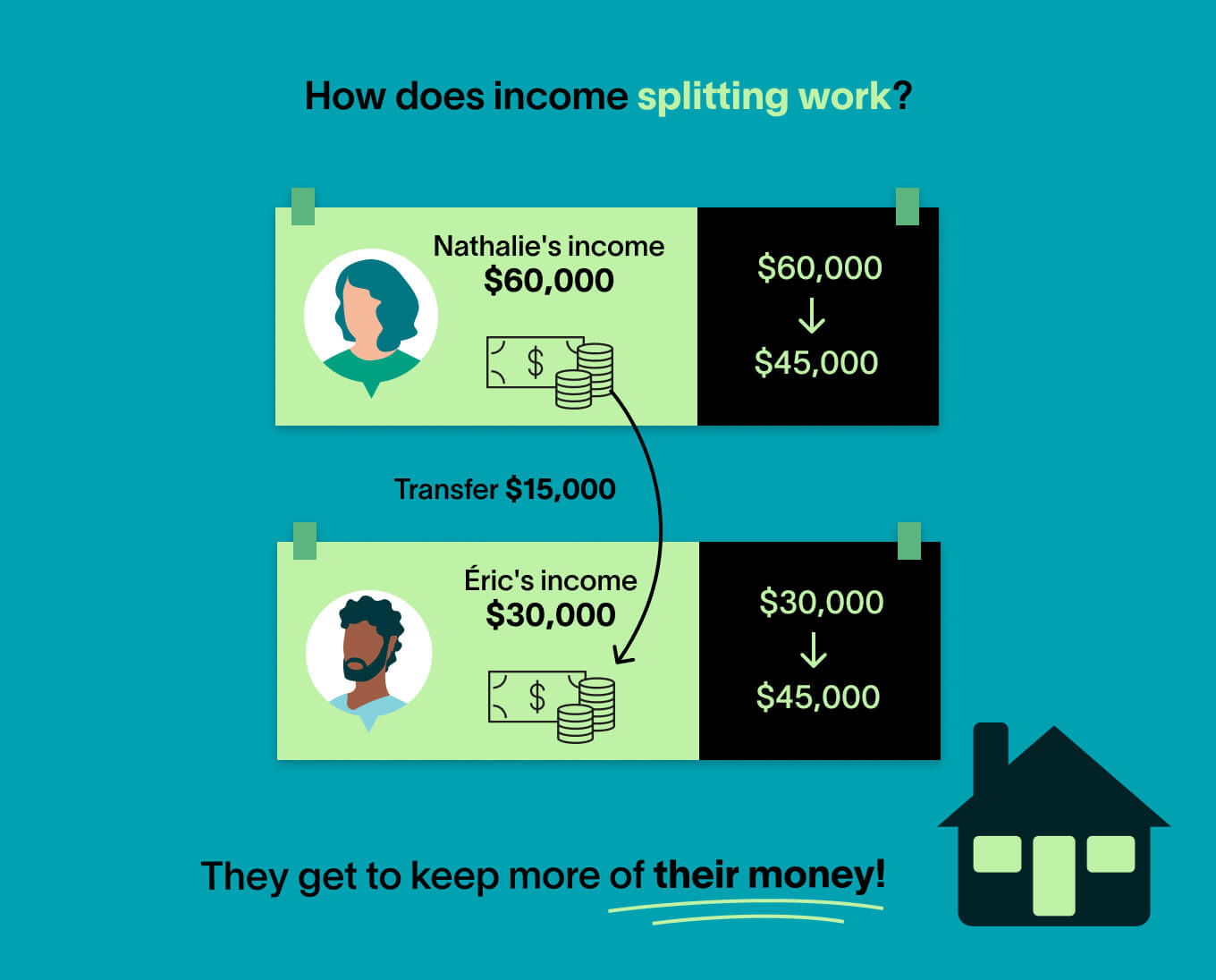

How does it work?

To better understand the impact on your portfolio, let's look at a numerical example.

- Nathalie receives $60,000 in eligible pension income. Her tax rate is higher than her partner's.

- Éric receives $30,000. His tax rate is therefore lower.

- At tax time, Nathalie decides to transfer $15,000 (a permissible amount since it's less than 50% of her pension) to Éric.

Result: Nathalie's taxes are based on $45,000 instead of $60,000, avoiding the most costly tax brackets. Eric's taxes are based on $45,000 as well (his $30,000 + Nathalie's $15,000), but since his rate is lower, the couple's total tax bill decreases. They get to keep more of their money!

To learn how to apply for income splitting, speak to a FlexiFonds mutual fund advisor. Our team can assess whether this strategy will work for you and direct you to the right resources.

Did you know?

Even if you're the one making the transfer, both partners must agree and sign the forms. This is a decision you make as a couple.

Who is eligible for pension income splitting?

To take advantage of pension income splitting, you and your partner must meet certain basic conditions:

- Be residents of Canada at the end of the year

- Be married or common-law partners. Common-law partners must have lived together for at least 12 consecutive months or have a child together.

- Not have lived apart for more than 90 days by the end of the year (except for medical or other admissible reasons)

- Receive eligible income

What income qualifies for pension income splitting?

Not all income is created equal! Rules under the federal and Québec systems differ slightly depending on your age.

If you are 65 or older, most of your pension income is eligible:

- Pension plan annuity (employer-sponsored pension fund)

- RRIF (registered retirement income fund) withdrawals

- Life annuity payments

- LIF (life income fund) withdrawals

If you're under 65, options are more limited. At the federal level, typically only a life annuity under a pension plan is eligible. In Québec, you must be 65 years old to split income.

Please note: Public pensions, such as the OAS (Old Age Security pension) and QPP (Québec Pension Plan) are not eligible for splitting. That said, the QPP has its own income splitting program. Managed by Retraite Québec, this program operates under different rules.

Start early, enjoy more!

It can be tempting to put off RRSP and RRIF withdrawals for as long as possible. However, gradual disbursement from the start of retirement is often the best way to ensure the lowest tax rates. Plus, converting your RRSPs to RRIFs at age 65 gives you access to the pension income credit (federal), retirement income credit (Québec), and pension income splitting.

We can help you

While splitting pension income can be a powerful strategy for paying your fair share of taxes, every couple's situation is unique. Our FlexiFonds mutual fund advisors can help you formulate a tax-advantaged strategy that's right for your family.

Ready to take action?

Planning your finances is easier than you think with My Game Plan, a simple and intuitive tool that helps you see things clearly. Get started today to take stock of your situation and receive personalized recommendations.