Between saving for retirement, your children's education, vacations, renovations, and inevitable contingencies, it can be hard to know where to focus your attention in the family budget. Especially when you consider that, according to several estimates, raising a child to the age of 18 can cost nearly $300,000! When life is expensive and resources are limited, how do you allocate your savings wisely?

Don't panic! We understand: You want the best for your family, but you can't do everything all at once. The important thing is to create a structured plan. Here's a guide to help you get clarity and set your priorities—one step at a time.

Define your savings capacity with the 50/30/20 rule

Before deciding where to put your money, you need to know how much you can save. To figure that out, budgeting is essential.

A simple and effective method to use is the 50/30/20 rule. It's an excellent starting point for balancing your budget and suggests dividing up your net income as follows:

- 50% for basic needs (housing, food, transportation, electricity)

- 30% for leisure activities and wants (outings, subscriptions, vacations)

- 20% for savings and debt repayment

If setting aside 20% of your net income seems unattainable right now, aim for the classic rule of saving 10% of your gross income. The important thing is to get started, whatever the amount. The habit matters more than the number!

Where should you put your money first?

Once you've determined your savings capacity, here's a logical sequence for optimizing every dollar, while protecting your family's future.

Priority 1: Build your emergency fund

This is the foundation for everything. Before you think about investing long term, make sure you have a financial cushion for unexpected expenses (job loss, car repairs, etc.).

- Objective: Cover three to six months of living expenses.

- Method: Use a high-interest savings account or a TFSA (Tax-Free Savings Account), as long as you can still access the money quickly (i.e., it's liquid) and without penalty.

Priority 2: Tackle "bad" debts

If you're carrying a balance on a credit card or personal loan with an interest rate above 8%, that's your priority number two.

As Sébastien Lafontaine, FlexiFonds mutual fund advisor and financial planner emphasizes:

"These debts limit the money available for savings. The sooner you pay them off, the sooner you can establish and grow your wealth."

Important nuance:

Your mortgage is generally not considered a bad debt. We'll come back to that below!

Priority 3: Take advantage of education grants (RESP)

If you have children, a Registered Education Savings Plan (RESP) is a must. As soon as your child has a social insurance number (SIN), you can set up a plan.

For every dollar you contribute, you can benefit from substantial government grants. Total federal and provincial grants can amount to up to 30% of your contribution, with a maximum of $750 per year (and a lifetime maximum of $7,200). Plus, if your income is more modest, the Canada Learning Bond can even add money to the plan without you having to contribute. It's excellent financial leverage and provides an unbeatable guaranteed return.

Priority 4: Prepare for retirement (RRSP or TFSA?)

This is the age-old dilemma. Here's how you can decide, based on your situation and financial outlook:

- If you have a modest income (or if you expect your income to increase significantly in the future):

A tax-free savings account (TFSA) is often preferable at first. Not only do TFSA withdrawals have no impact on government benefits—unlike RRSP (Registered Retirement Savings Plan) withdrawals—they also provide valuable flexibility. You can accumulate your savings in a TFSA and, later, when your income is higher, you can consider transferring those amounts (or make new contributions) to an RRSP to maximize your tax deduction when your tax rate is higher.

- If you have a high income:

An RRSP becomes advantageous. By contributing to an RRSP, you lower your taxable income, so you pay less tax today and your savings grow tax-free. The higher your income is, the higher your marginal tax bracket will be, and the greater the tax savings generated by your RRSP contribution. This is a powerful option if you're already in a high tax bracket.

The leverage effect for families

Sébastien Lafontaine points out a key advantage of RRSPs for parents: "When you contribute to an RRSP, it reduces your family net income. As a result, it can increase your access to important social programs, such as the Canada child benefit or the tax credit for childcare expenses."

Get even more with the RRSP+

Subscribing to Fonds de solidarité FTQ shares can give you access to a 30% tax credit,[1] in addition to the standard RRSP deduction. The RRSP+ is a powerful tool for increasing your tax refund, which you can then reinvest—in your children's RESP, for example!

Priority 5: Finance your medium-term projects

Once you've set aside money for retirement and education, think about your medium-term projects, like doing renovations, travelling, or buying a new car. A TFSA is the ideal tool for growing your money tax-free while keeping it available.

Tip:

Since you'll need the money fairly soon (time horizon of less than five years), choose your investments carefully. Opt for a balance between security and growth, so the money is there when you need it. A mutual fund advisor can help you identify your investor profile based on your situation. Learn more about investment risk.

Should you invest before paying off your mortgage?

Should you try to pay off your house faster? Not necessarily, if it's at the expense of saving for retirement or education.

"You have choices to make. A principal residence is an asset that increases in value over the long term, but it's less liquid. It's not a bad debt. However, the money you put toward paying off your mortgage is not invested in other investments that could yield a higher return," explains Sébastien Lafontaine.

Not to mention the tax advantages you miss out on if you focus on paying off your mortgage instead of contributing to your RRSP, for example. If you want to pay off your mortgage faster, you can opt for an accelerated payment schedule (e.g., paying every two weeks instead of every month), or use your tax refund to reduce your mortgage balance. Basically, the important thing is not to restrict your savings capacity.

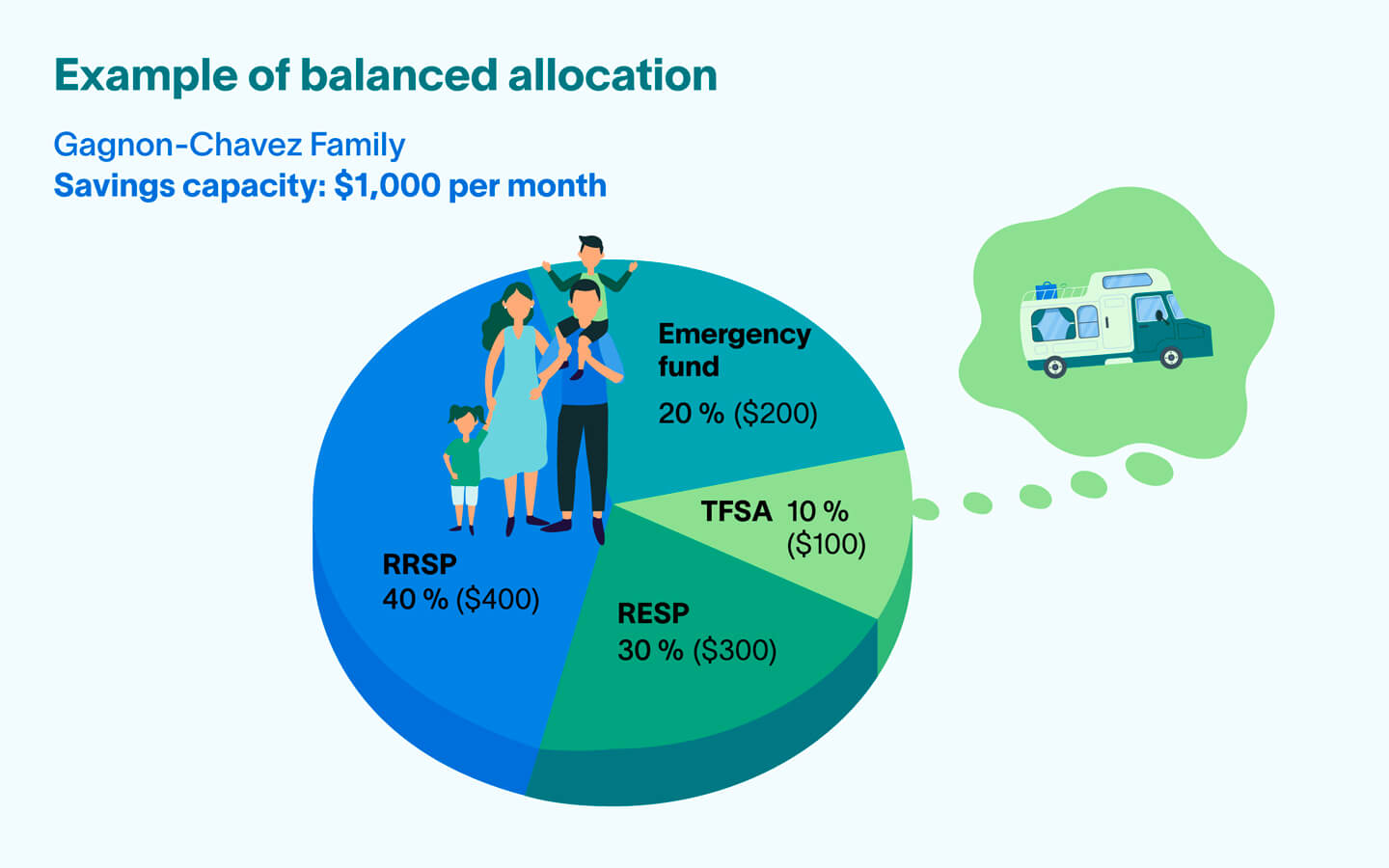

Case study: The Gagnon–Chavez family

Let's take a look at how this applies in real life.

- Profile: Two adults, two young children

- Gross family income (after taxes): $120,000

- Situation: Homeowners, mortgage in progress, no consumer debt

- Savings capacity: $1,000 per month (about 10% of gross income)

Example of balanced allocation:

- $200/month in the emergency fund (up to 3 months' salary)

- $300/month in the RESP (to maximize grants as much as possible)

- $400/month in an RRSP, like the RRSP+ (for tax savings and retirement)

- $100/month in a TFSA (for their upcoming summer camping vacation)

What if the budget were tighter?

If this family could save just $500 a month, the strategy would change: They should prioritize their emergency fund until it reaches the desired amount. Without that safety net, they risk being in a tight spot financially due to any little setback. Next, they should pay off any high-interest debts, then divide what's left between saving for education and retirement.

Three tips to help you stay on track

- Automate everything: Systematic savings (automatic withdrawals) reduce your mental load. If it's not in your chequing account, you won't spend it!

- The "ricochet" strategy: Use the tax refund generated by your RRSP contributions to fill up your children's RESP or pay down debt. It's a smart way to make every dollar go further.

- Get your kids involved: Explain your choices to them (why you're putting money aside for later). That will give them a sound financial understanding for the future.

Need to paint a clearer picture?

Try the My Game Plan tool to map out your finances! It's simple and intuitive to use, and it helps you visualize all your savings, test different scenarios, and get personalized recommendations to make your projects a reality.

A stable future, one step at a time

In short, there's no one-size-fits-all solution for budgeting and saving, but there are logical principles that have stood the test of time. By structuring your priorities, you'll build a stable future for the whole family—without giving up all the pleasures you enjoy today.