Many people claim their benefits as soon as they become eligible; it can seem like the obvious choice. But when it comes to retirement planning, patience can pay off. If your financial situation allows it, delaying your public pensions is one of the most effective ways to secure higher guaranteed lifetime income and avoid leaving $100,000 or more on the table.

QPP and OAS: Understanding how they work so you can make the right decision

Before pulling out the calculator, let's review the two main components of Québec's public retirement system: the Québec Pension Plan (QPP) and Old age Security (OAS), the federal pension.

These pensions provide income for the rest of your life, but how much you receive depends on when you start collecting. The system is actually set up to reward those who delay.

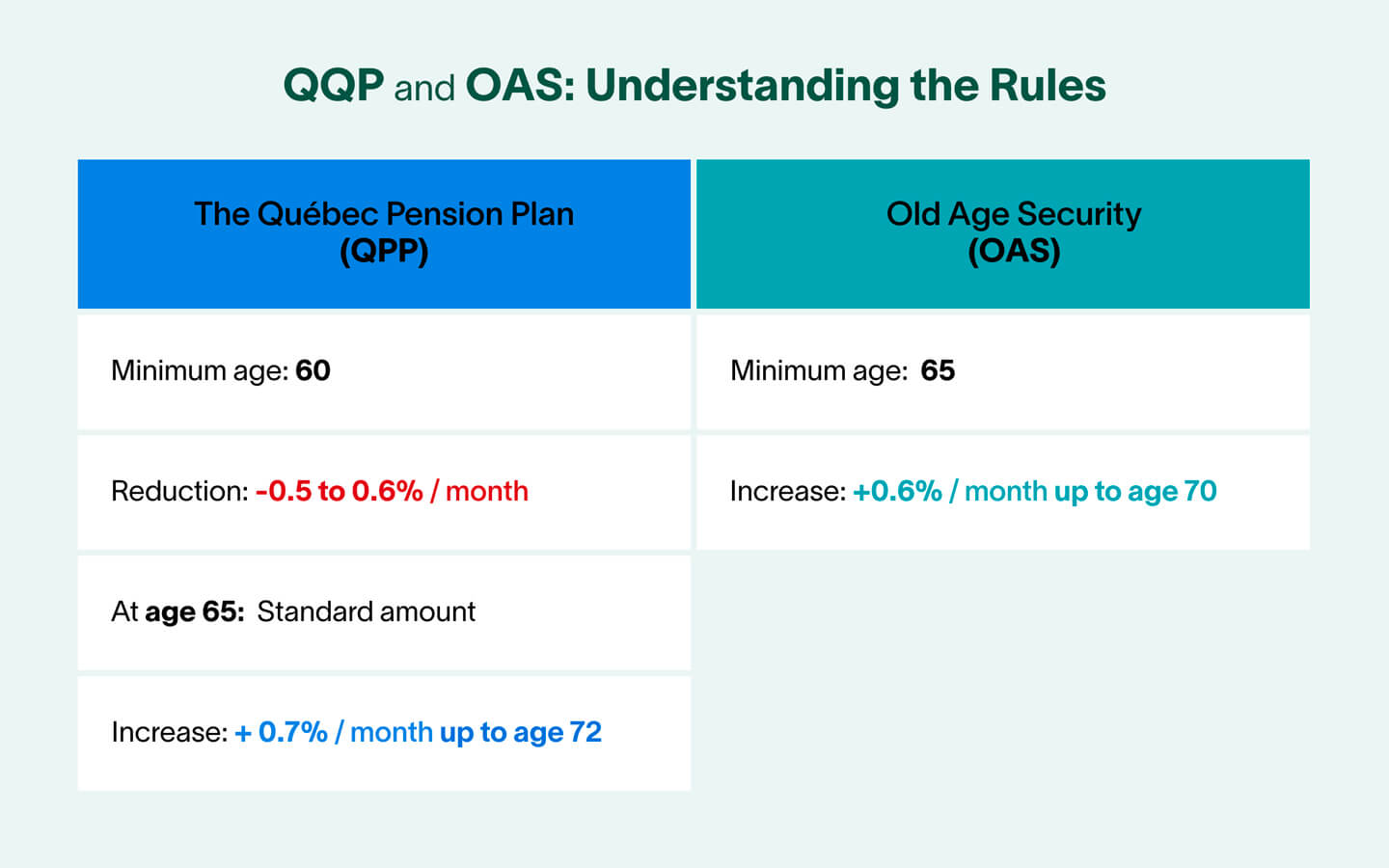

- The Québec Pension Plan (QPP): You can begin receiving your pension as early as 60, but the standard retirement age is 65. Claiming before 65 reduces your pension by 0.5% to 0.6% for each month taken early. On the other hand, if you wait past 65, your pension increases by 0.7% for each month of delay, up to age 72.

- OAS (Old age Security): You can start receiving OAS at age 65. However, you may defer it until age 70, which increases your monthly payment by 0.6% for each month you delay.

Waiting: How much of a difference does it make?

This is where the numbers matter—and they're often misunderstood. Delaying your pension can have a significant impact on your long-term income.

"Ideally, when it's feasible, we recommend not claiming your benefits before age 65. The penalty for starting early is steep, and the increase for waiting is substantial."

— Mélanie Poupart, FlexiFonds mutual fund advisor

Of course, life doesn't always follow an Excel spreadsheet. "These days, people are facing layoffs, restructurings, and so on," Mélanie says. "If someone develops a serious illness late in their career, has a reduced life expectancy, or has to leave their job early with no other income, they don't really have a choice. So they take their pensions at 60—and that's okay."

However, for those who are still working or who have personal savings (RRSPs, TFSAs), claiming too early can be costly. "For many of the people I speak with, if they're still working but decide to take their QPP at 60 in order to "enjoy it," they're leaving a lot of money on the table. It not only increases their taxes because the pension is added to their employment income, it can significantly reduce their monthly income later in life, at age 75 or 85," she says.

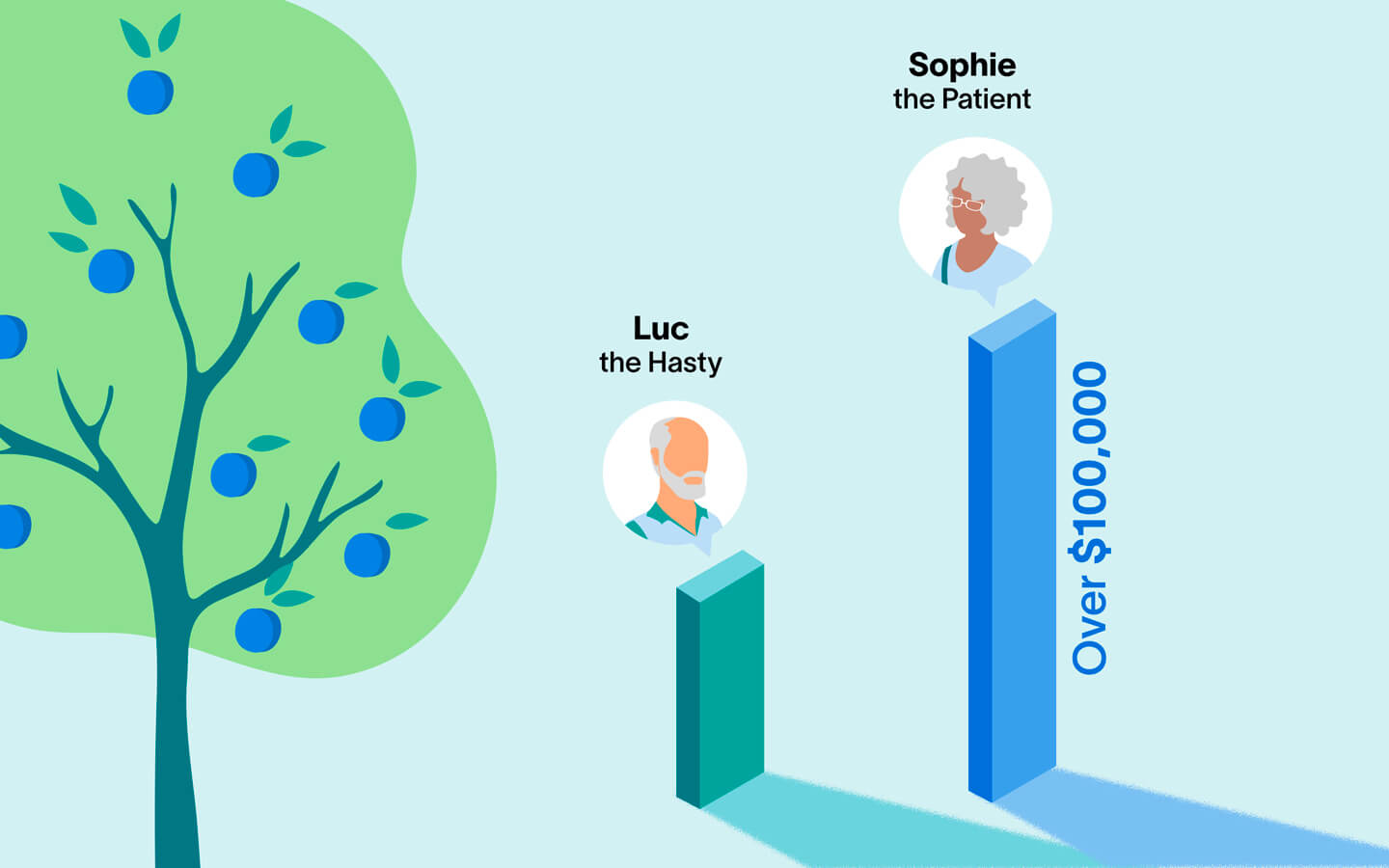

A $100,000 gain: Luc and Sophie's story

To illustrate the real financial impact, let's compare two colleagues with similar salaries who retire at the same time but choose different strategies.

Meet Luc and Sophie. Both qualify for the maximum Québec Pension Plan (QPP) benefit and the Old age Security (OAS) pension. They are both 60 years old and in excellent health.

Luc's strategy (claiming early): Luc is afraid of "missing out." He wants his money as soon as possible. He decides to claim his QPP at 60 and his OAS at 65. As a result, his QPP pension is permanently reduced by 36% compared with what he would have received at 65. He starts receiving payments as soon as he's eligible, but they are relatively low.

Sophie's strategy (being patient): Sophia reviews the numbers with an advisor. She chooses to live off her RRSPs for a few years and waits until age 70 to claim her QPP and OAS. As a result, at 70, her QPP benefit is 42% higher than it would have been at 65, and her OAS is 36% higher. Her monthly payments are nearly double Luc's.

The bottom line:

If Luc and Sophie both live to age 85, the cumulative difference in what they receive is striking. Here is a detailed comparison of their monthly benefits and lifetime totals.

Monthly difference

| Luc | Sophie | Variance | |

|---|---|---|---|

| QPP at start (per month) | $965 | $2,141 | +$1,176 |

| OAS at start (per month) | $742 | $1,010 | +$268 |

| Total per month | $1,707 | $3,151 | +$1,444 |

Total difference over their lifetime

| Luc | Sophie | Variance | |

|---|---|---|---|

| QPP lifetime total | $289,500 | $385,380 | +$95,880 |

| OAS lifetime total | $186,984 | $193,920 | +$6,936 |

| Total | $476,484 | $579,300 | +$102,816 |

Notes on the calculations

- OAS lifetime totals include the 10% increase starting at age 75.

- Amounts are expressed in today's dollars.

- Calculations are based on 2026 data and do not account for annual cost-of-living adjustments or income taxes.

The difference: Sophie receives over $100,000 more than Luc

Luc begins receiving his pensions ten years earlier, but Sophie comes out ahead in the long run. If she lives to 85, she will have received more than $100,000 in additional guaranteed income.

In other words, her patience pays off. She effectively gave herself an extra $100,000 through careful planning.

The longevity risk: Debunking the myth

The main argument against delaying your pensions often sounds like this: "What if I die at 69? I'll lose all my benefits!" It's a legitimate fear, but mathematically, the greater risk is the opposite one.

People often talk about market risks, but you don't hear as much about longevity risk: the risk of outliving your personal savings. Life expectancy in Québec continues to rise. If you're healthy at 60, there is a strong probability that you will live past 85.

Unlike RRSPs, which can be depleted if you live to 100, QPP and OAS provide guaranteed, indexed income for life.

Nasser Mama, FlexiFonds mutual fund advisor and financial planner, explains:

"Government pensions are one of the most effective ways to secure enhanced, indexed income for life, if your financial situation allows. They provide income that is protected from market fluctuations."

By deferring your pensions, you are effectively strengthening your protection against longevity risk. If you live a long life, you come out ahead. If you pass away early, you may have received less overall—but you also won't outlive your savings. The goal is to ensure financial security for "your future you" at age 90.

Protection against inflation

Another often-overlooked factor is indexing. Public pensions are adjusted to reflect changes in the cost of living. If inflation rises, your QPP and OAS benefits rise as well. By delaying your pension, you increase the base amount to which these adjustments apply. For example, a 2% increase on a $1,500 monthly benefit is significantly more than 2% on an $800 benefit. Deferring your pension therefore strengthens your long-term protection against inflation and helps preserve your purchasing power over time.

The financial bridge: What will you live on while you wait?

Delaying your pensions raises a practical question: if you don't claim your government benefits at 60 or 65, how will you cover living expenses? The answer is a withdrawal plan, which acts as a financial bridge.

The idea is to use your personal savings to bridge the gap until your public pensions begin.

Sébastien Lafontaine, FlexiFonds mutual fund advisor and financial planner, explains: "You can take advantage of the period before you start receiving government pensions to withdraw from your RRSP or RRIF, since your tax rate is typically lower."

Here's how the strategy works in detail:

- Drawing down RRSPs/RRIFs (ages 60–70): "The idea is to withdraw the most heavily taxed funds when your income is lowest," says Sébastien. Between 60 and 70, if you haven't started your pensions, your taxable income is likely lower. This makes it an ideal time to withdraw from your RRSPs or RRIFs at a lower marginal tax rate than you would face at 72, when QPP and OAS income is added.

- Avoiding OAS clawback: For higher-income retirees, delaying RRSP withdrawals too long can push net income above the 2026 threshold (about $95,000), meaning part of the OAS must be repaid. By withdrawing earlier, you reduce this risk.

- The TFSA-pension combination (age 70 and over): Once your government pensions start, you can supplement your income with TFSA withdrawals. Why? TFSA withdrawals do not count toward net income for tax purposes, so your OAS remains protected.

It's a balancing act: drawing from taxable accounts earlier allows your pensions to grow more before you claim them. This approach can be beneficial, but it isn't suitable for everyone—an advisor can help determine if it fits your situation.

My Game Plan: Test different scenarios

Every retirement is unique. General numbers are helpful, but your personal numbers matter most. Does deferring your pension benefit your situation? Does your spouse have a large pension? Is your life expectancy lower than average?

Run simulations in My Game Plan, a financial planning tool that uses your actual data. The tool is available free to anyone with savings at the Fonds or FlexiFonds products through their online account.

A few clicks allow you to explore different scenarios:

- "What happens to my net income at age 85 if I claim my QPP at 65 instead of 70?"

- "Are my current savings enough to cover my expenses if I delay my pensions?"

- "How much do I need to save if I want to claim my pensions at 70?"

The tool provides personalized projections and recommendations to help you achieve your retirement goals and projects, whether you want to renovate your home or simply rest easy at night.

A decision that pays off in the long run

Delaying your pensions is not a choice to take lightly, but it can be a winning strategy. By covering expenses with your own savings for a few years, you protect your future income against inflation and gain lasting financial security.

However, the best strategy is the one that fits your situation. Don't hesitate to talk to our FlexiFonds advisory team to help you solidify your plan.